The S&P 500 spent the year making new all time highs soaring nearly 30% on the year.

After its major halving event (cutting rewards to miners) Bitcoin powered into the end of the year crashing through the $100,000 level.

And in yet another Festivus feat of strength, the Nasdaq Composite (2,500 shares strong) blasted through the 20,000 level.

In truth, much of this year’s performance in the stock market has been the result of the mega-cap sector: Those trillion dollar-plus market cap companies heavily involved in the AI boom. If you factor out their weighting in the S&P 500, the index’s performance on the year is cut by about half. (It’s only up about 15% which is more in line with the small-cap Russell 2000 has done.)

But alternate measures aside, the AI sector is booming and appears it will keep booming for the foreseeable future.

This week’s stock spotlight is on one of those drivers.

The Boom in Broadcom

Broadcom Inc. (AVGO) is one of the tech stocks that’s muscling its way into the Mag-level club having just eclipsed $1 trillion in market cap.

Broadcom is involved in both the semiconductor industry as well as infrastructure software — namely software in the cloud computing biz.

Last week, AVGO released its fourth quarter earnings. CNBC reported:

Broadcom reported better-than-expected fourth-quarter earnings on Thursday and said artificial intelligence revenue for the year more than tripled.

AI revenue had reached $6 billion from less than $2 billion at the beginning of the year.

Add to that the fact that revenue from its chips segment also grew 12% year-over-year and you’ve got a damn hot stock.

Broadcom Inc. (AVGO) YTD

Source: Barchart.com

The market literally stampeded on board. And this is no doubt excellent news for the company.

But there are two things investors should take note of.

First, you can see a similar gap higher back during its June earnings release. Prices followed through for a couple sessions, but then consolidated over 20% lower, testing the stock’s 200-day moving average.

The other thing you’d want to look at is the company’s valuation at current levels. At these post-gap prices, shares are trading at a P/E of 195. (That means you’re paying $195 for every $1 of earnings.)

A lot of tech companies have gotten pretty heady in the past. But things have settled to more realistic valuations. META’s P/E is only around 29. MSFT is only 36. Even the big dog in the AI pack — NVDA — is only sporting a P/E of 53.

Broadcom has moved into some lofty valuations.

And while the future may be bright for this newly minted $1 trillion behemoth, investors might do well to exercise some patience when looking at it.

“All the Whos down in Whoville liked Christmas a lot.

But the Grinch, who lived just north of Whoville, did not!”

– Dr. Seuss

The annual holiday classic, that we’ve all seen a million times, tells the story of a nasty green cave dweller who tries to stop Christmas.

Despite the fact he eventually learns the true meaning of Christmas and saves the day, his name has become synonymous with being cynical or mean-spirited.

Well, since the holiday season is at hand, we want to say up front that we really don’t mean to be a Grinch about the markets.

But given we feel it’s our duty to show our readers the unvarnished investing truth, here’s a development you need to know…

Recalling the “Value Master”

A couple weeks back, we took note of the fact that none other than Warren Buffett — mister buy and die — had become a net seller in the stock market.

Buffett, who still actively manages Berkshires’ portfolio, has been a net seller of stocks for the past eight quarters, significantly rearranging his portfolio. …

Add it all up and Buffett has raised Berkshire’s cash position to $320 billion versus just $272 billion in stocks.

We speculated on the reasons for this notable shift in sentiment:

Is the Oracle calling a top? It’s certainly not impossible. Buffett is the king of buying value — great companies fairly priced. If valuations are exceeding what he deems reasonable, he may be building a cash store to take advantage of a major correction.

We also noted that Buffett is not a market timer. So the fact that he’s unloading now doesn’t suggest that anything is imminent. Better to be out when you want to be in instead of in when you want to be out.

But given our speculation, we found a recent analysis of the market’s overall valuation to be worth noting. But first…

A Little Primer On Valuation

When you buy a stock, you’re basically buying a piece of the company’s expected future earnings. And the price you pay today should reflect a discounted value of that. So in basic terms, price should be a fair reflection of value. But that’s not always the case.

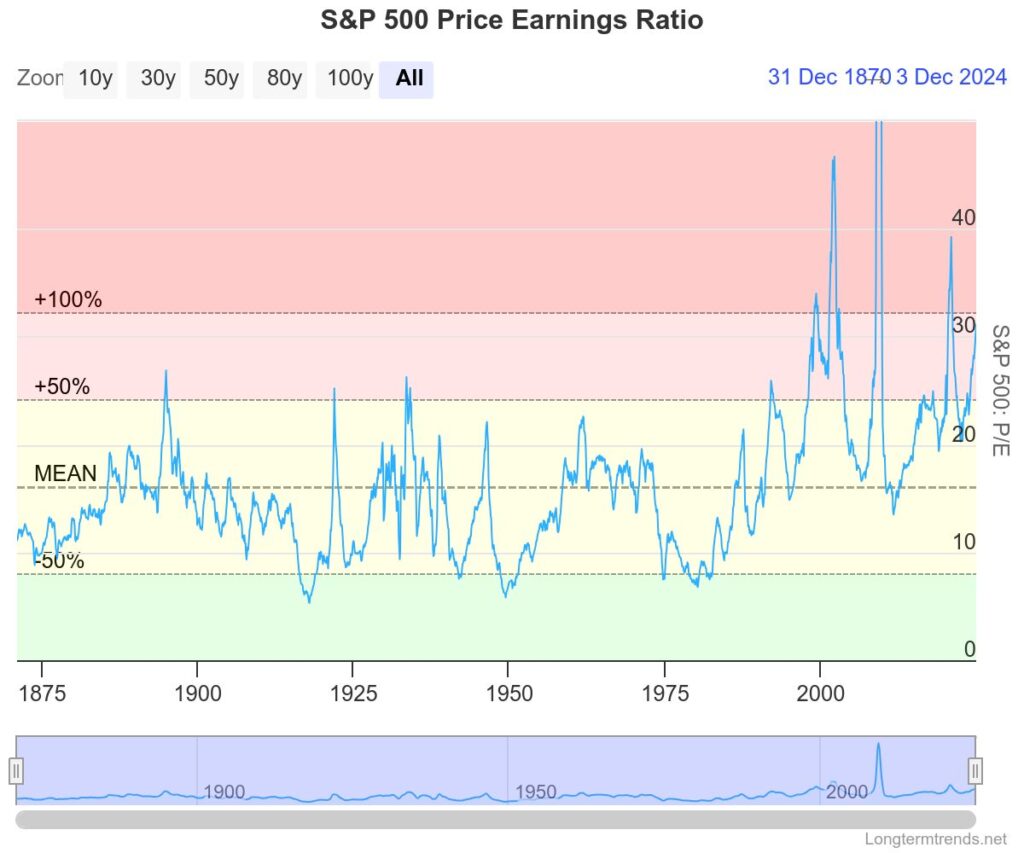

Comparing the price of a company’s stock to its earnings (price-earnings or P/E ratio) is the most common way of establishing valuation. Below is an historical chart of the P/E ratio of the S&P 500:

You can see that for over 100 years, valuations basically oscillated around the long-term mean with a dip 50% below indicating undervalued and rise to 50% above indicating overvalued. Then, however, came the tech bubble and valuations became both extreme and extremely volatile.

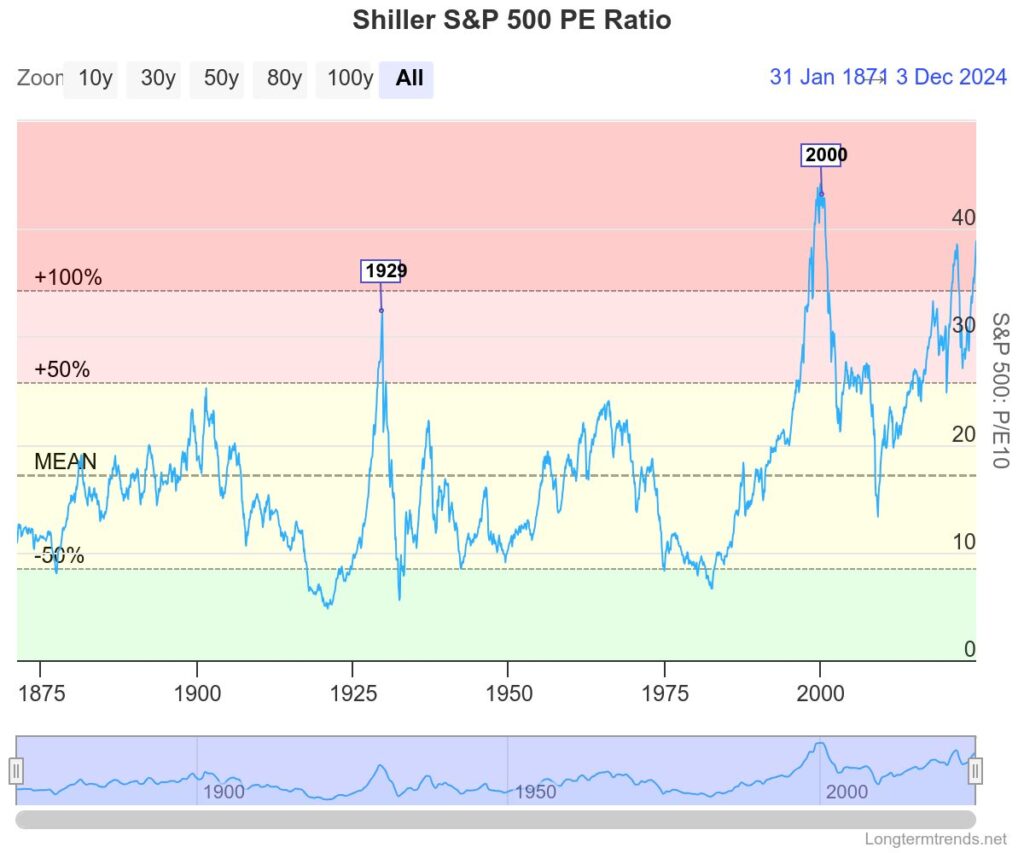

Another, more smoothed measure, is known as the cyclically-adjusted price-earnings (CAPE) ratio. (It’s also known as the Shiller PE Ratio for the economist Robert Shiller who invented it.) This ratio measures price to earnings except instead of using a single year of earnings, it uses average real earnings over a 10-year period. This smooths out volatility as a result of business cycles.

You can see this measure smoothed things out considerably leaving only two overvaluation spikes: before the crash of 1929 and the bust that followed the tech bubble… until today.

Today valuations according to the Shiller ratio are at their second highest levels in history.

But there’s yet one more level of smoothing that can be done…

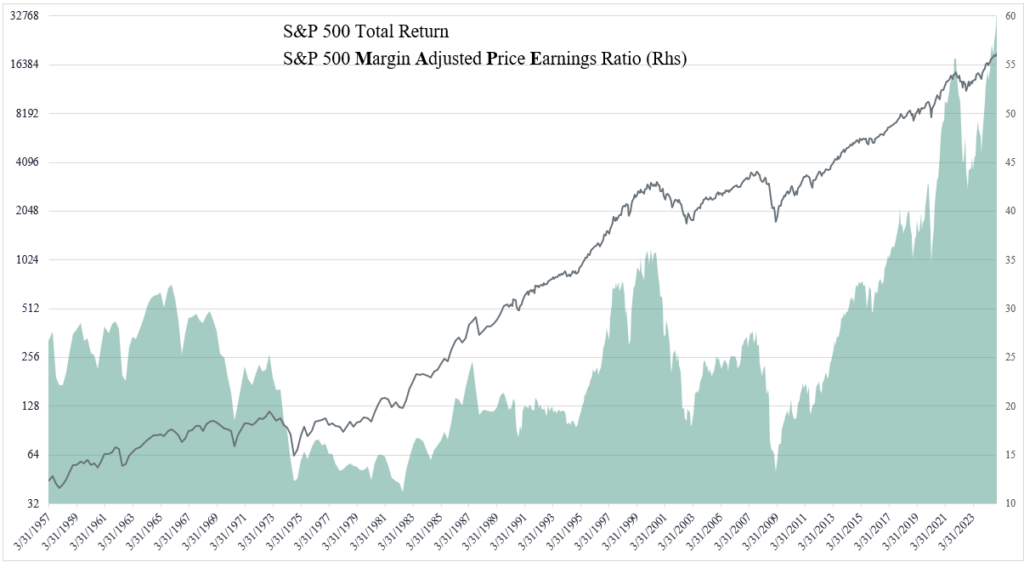

It comes from Damien Cleusix of QuantasticWorld and it’s called the margin-adjusted, cyclically-adjusted price-earning ratio (MAPE).

MAPE factors in and adjusts for the level of profit margins embedded in the valuation calculation. And by this measure the market isn’t just overvalued… It’s insanely overvalued. According to Cleusix “the US stock market is the most overvalued it has ever been.”

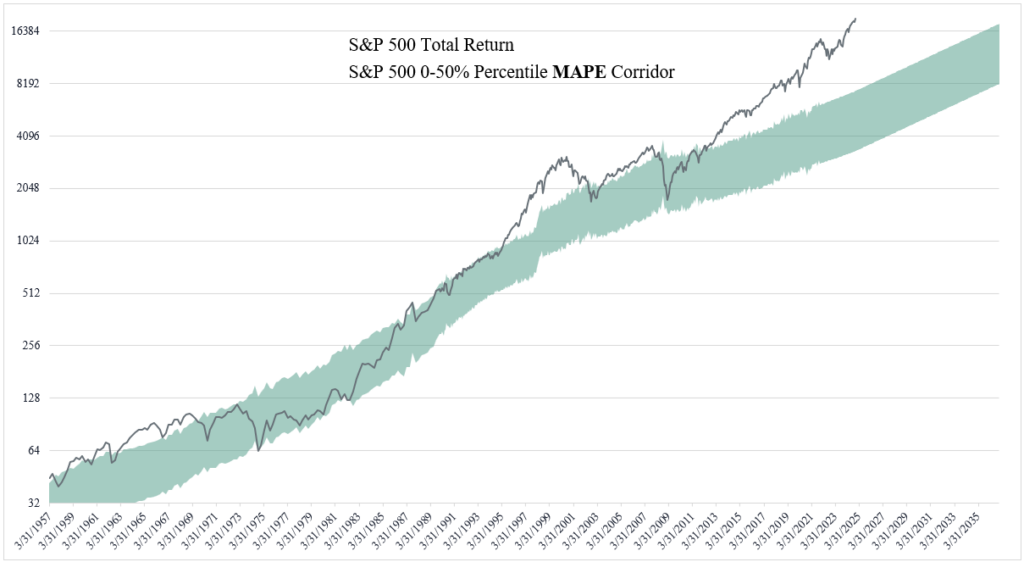

Looking at this chart, the sky-high valuations (the level traced in green) are obvious. Further, if you construct a band with boundaries between the 0 and 50 percentiles of historical MAPE, this is what you get:

The S&P 500 is currently almost 400% above the level corresponding to a bottom MAPE and 130% above the 50% percentile MAPE history.

Valuations at the high end of any measure suggest that an investment is “priced for perfection” — that earnings and growth will continue ad infinitum. And that leaves the door open for any kind of disappointment to send prices plummeting back to more “reasonable” valuations.

Like we said, we don’t want to be Grinchy this close to the holidays. But being aware of the potential threats to the market (and the bad news that could result) is the key to actually having a merrier Christmas!

The Fed has officially embarked on its quest for the holy grail of monetary policy…

Having slain the inflation monster with restrictive rates of 5.5% (or so they say) they must now start easing off the brakes so the rest of the economy doesn’t sputter and die.

The problem is, as Chairman Powell has admitted over and over, they have no idea what “neutral” actually is. (But they assure us, they’ll know it when they see it.)

And despite not knowing where they’re headed, they launched their effort by slashing their target rate by 50 basis points. Pretty much as large as they could go without sparking some panic in the market.

The market, which had been in a solid uptrend since the low in October 2022, driven largely by mega-cap AI stocks, celebrated by continuing its rally.

This policy reversal by the Fed is something the market has been anticipating for some time. And now that the easing cycle is underway, it should continue to please those big players driving the market.

But it should also benefit another segment of the market that has been lagging. And that creates an opportunity for investors…

Rise of the Small Caps

Since the low in October 2022, small cap companies have lagged the bigger players in the market. Take a look at the chart below…

S&P 500 vs Russell 2000

Source: Barchart

You can see tightly related performance of both the S&P 500 (an index dominated by mega-cap companies) and the Russell 2000 (an index of small-cap companies) into the 2022 low.

Once mega-AI stocks began to drive the rally, the bigger better capitalized stocks took off. Smaller cap stocks, on the other hand, struggled to keep up lagging by over 20%.

That’s one sector that had been significantly impacted by the Fed’s tightening cycle. Now that’s very likely to change.

Why Small-Caps Love Lower Rates

Small cap companies are typically more sensitive to interest rates. One reason is that they tend to be more reliant on external financing to fund their operations and growth.

Huge companies like Alphabet, Amazon, Microsoft all have massive cash reserves they can fall back on to fund their strategic plans. Tens of billions have been spent by big tech from their war chests on AI development.

But many smaller companies, companies with market caps in the lower billion dollar range, don’t have that kind of financial ammo. They have to keep their eyes on operations. That means strategic borrowing is much more critical when it comes to things like financing growth and innovation.

Another reason is bottom line profitability.

Smaller-cap companies generally have smaller profit margins than their bigger capitalized cousins. And a higher cost of capital (what they pay to borrow) tends to take a significant bite out of their already-thin bottom line.

With the Fed moving to ease, lower financing costs will ultimately boost many small-cap companies’ bottom lines making them more profitable companies.

And of course, that leads to a third factor in bolstering the fortunes of the small-cap crowd — more profitable companies are more attractive to investors.

Lower interest rates, from an investor perspective, tends to generate what’s known as a “risk on” investment environment. One where funds and other institutional investors will leverage their portfolios by borrowing money to invest in companies they feel have potential for significant returns.

And companies that have the potential for significant returns? Well they’re generally the ones that are undervalued or have been lagging the broader market.

Right now, that’s the small cap sector.

Looking at the chart above, the small-cap sector as a whole has significant room to actually outperform larger-cap competitors.

Some small caps will do better than others. But right now may be the time for savvy investors to start scanning the small-cap universe for significant opportunities.

What a week for tech stocks.

A sci-fi-level technology known as “quantum computing” is fast becoming a reality, and certain stocks in the field have seen explosive gains in the last week.

Quantum computing is based on the science of quantum mechanics — a theory in physics that deals with our world at the subatomic level. And things at the subatomic level operate a little differently than we understand them.

Where bits in the observable world are only 0’s or 1’s, bits in the quantum world (also known as “qubits”) can be 0’s, 1’s or 0’s and 1’s simultaneously.

If that concept makes your head spin, don’t worry about it; you don’t have to completely understand a new technology to potentially make a ton of money investing in it.

You can bet that most early IBM investors didn’t know exactly how its revolutionary, world-changing microprocessor technology worked … but those investors were able to see extraordinary gains as computing took over the world.

This new quantum computing tech has the same world-changing potential (maybe even more) as the microprocessor — and this rapidly developing technology is leading to some exciting opportunities for investors.

Here are three ways to play the trend … plus one bonus “sleeper” play for investors looking for aggressive growth potential.

Quantum Play #1: The 800-Pound Gorilla

For investors interested in doing some more due diligence in the area of quantum computing, here are three places to look for opportunity.

For those looking for the safest play in this up and coming field, look no further than Google (GOOG).

Google has been at the leading edge of quantum computing for years. And recently they just announced a major breakthrough in their technology.

Source: Nature

One of the challenges that comes with this new quantum tech is the ability to scale it. Adding more and more qubits to a process increases the number of errors that are likely to occur. (This has been a challenge in the field since 1995.)

It appears that Google has finally designed a breakthrough with its latest quantum processor known as Willow. According to an article in Nature Magazine…

Researchers at Google have built a chip that has enabled them to demonstrate the first ‘below threshold’ quantum calculations — a key milestone in the quest to build quantum computers that are accurate enough to be useful.

“Below threshold” calculations drive the number of errors down, while scaling up the number of qubits processed.

According to a recent blog post by Hartmut Neven, the founder of Google Quantum AI:

Willow performed a standard benchmark computation in under five minutes that would take one of today’s fastest supercomputers 10 septillion (that is, 1025) years — a number that vastly exceeds the age of the Universe.

You read that right. Willow did in five minutes what it would take the most advanced supercomputer today 10,000,000,000,000,000,000,000,000 years to do.

And it did it while reducing the number of errors that occurred.

Needless to say, this is a HUGE breakthrough for Google.

Quantum Play #2: Leveraging Light Waves

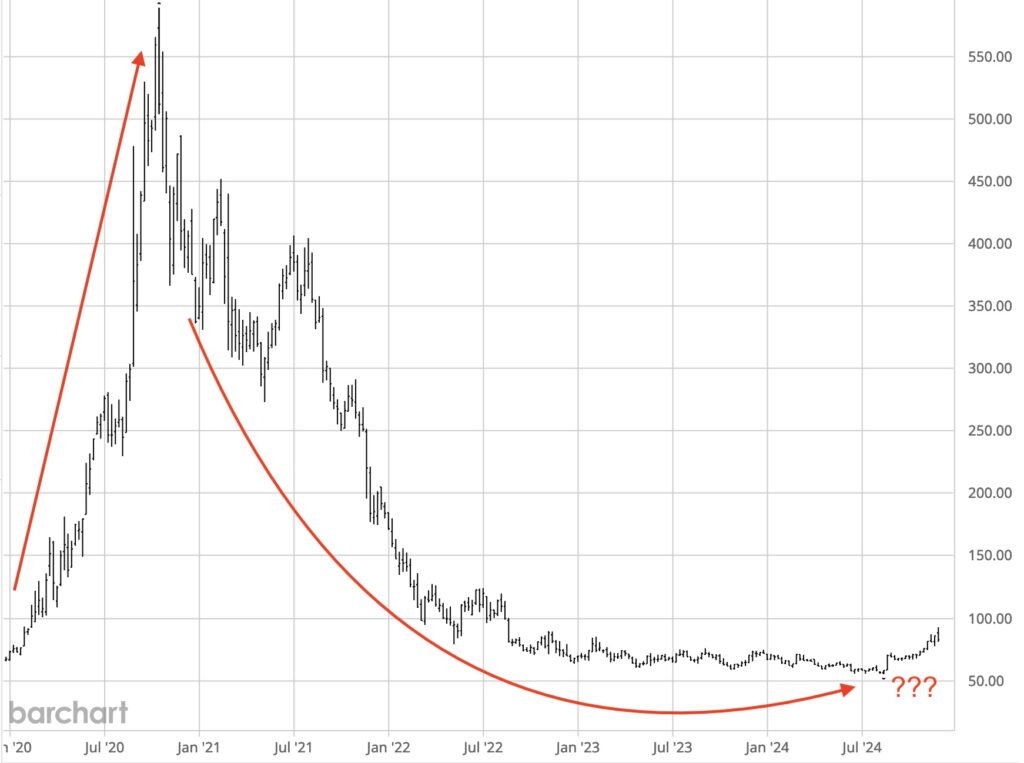

For those looking for a more aggressive play, look no further than what’s becoming the hottest quantum stock in the market today… Quantum Computing Inc. (QUBT).

While Google is busy scaling, QCi has been attempting to carve out its own niche in the quantum field using a technology known as thin-film lithium niobate (TFLN) chips that leverage nonlinear quantum optics.

That’s a mouthful, but what it basically means is that QCi’s technology uses light to generate qubits. Where a computer today can only understand bits where a light is on or off, qubits generated from light can act like a dimmer switch. They can be on, off or anything in between. Nonlinear quantum optics is the science that allows their technology to create and work with these qubits.

While the company is relatively small — its market cap is only around $2 billion — it has recently announced multiple orders for their tech.

The first came from an unnamed “prominent research and technology institute based in Asia.” A week later they announced a second purchase order from the University of Texas at Austin.

And even more recently…

Source: PR Newswire

While the specifics of the orders weren’t completely clear in the press releases, the company’s share price exploded over 1,100% in the last month on the news.

Quantum Play #3: The Wild Card

Investors interested in more of a pure quantum play could look into Rigetti Computing (NASDAQ: RGTI).

The California-based quantum computing pioneer had a lot to be thankful for in late November as its stock popped following news that it had raised $100 million in a direct offering.

And that wasn’t the only good news coming out of Rigetti this year. It also announced that it had installed a 24-qubit quantum computer in the UK’s National Quantum Computing Centre.

As of this writing, the company’s stock is up more than 928.85% over the last 6 months, but analysts are mixed as to whether Rigetti is hitting a roof or if the company still has room to grow.

But with $100.5 million in cash reserves, growing partnerships worldwide, and fresh interest in its industry-leading quantum services, Rigetti could make a very compelling investment opportunity for the right investor.

Bonus Play: The Quantum “Sleeper”

Finally, if you’re an investor with a bit more risk appetite looking for an under-the-radar small-cap company that’s targeting a critical area in the quantum field, you might want to investigate Scope Technologies Corp. (OTCQB: SCPCF; CSE: SCPE).

Scope Technologies is a Canadian-based company that has developed, among other things, quantum-proof encryption technology.

This is no small area when it comes to the prospects of quantum computing. The prospect of calculating at quantum speeds offers the potential for amazing benefits. But it also brings with it the potential for enormous threats.

Consider what Google’s Willow chip just did — it performed a benchmark calculation in five minutes that an advanced supercomputer would take 10 septillion years to do.

Now think of that in terms of today’s computer security.

Cybersecurity company Hive Systems created a table estimating how long it would take a sophisticated hacker today to crack passwords of various lengths and complexities…

Source: Tech.com

The bottom right corner shows the strongest password combination would take roughly 26 trillion years to beat.

That’s probably two-and-a-half minutes in Willow’s quantum time.

As the power of quantum computing becomes more and more mainstream, the need for equally powerful cyber defenses will skyrocket.

Streetlight Confidential Senior Editor Tim Collins has put together an in depth research report on the topic that you can access here.

Scope Technologies is a small firm — only about $45 million as of this writing — and, unlike the other stocks listed above, its stock hasn’t seen a ton of upward momentum yet. But the company has great potential in an area that will be more and more critical as this technology evolves.

AI may be the tech darling of the day, the future of tech (and investors’ bottom lines) is shaping up to be in the quantum realm.

Washouts happen.

But ultimately they can be for the good.

Take Cisco Systems.

Back during the 90s tech boom, Cisco exploded becoming priced so far ahead of its earnings, that after it got its bubble comeuppance it never regained its previous highs. Still, the company bounced back, grew steadily and in early 2011 began paying a dividend. It went from being a superstar growth stock to a reliable dividend payer.

Cisco Systems (CSCO)

Source: Barchart.com

And while the company still hasn’t rebounded all the way to its all-time high, it has experienced a solid bullish trend from its lows.

Cisco is now a good stock to own.

Today, another of the pandemic darlings may be getting ready to rise from the ashes.

Is Zoom Ready to Boom Again?

Zoom Communications (ZM) — formerly Zoom Video Communications (more on that in a second) — could be repositioning itself to a similar end.

During its pandemic heyday, it was adopted as a major growth stock — a company with massive growth potential. It traded from an IPO value of around $63 to a staggering $550-plus in a matter of months.

A little too far out over its skis, the company crashed back to reality.

These days, however, the company has been performing well financially. Its most recent earnings report saw the company beat estimates on both earnings per share ($1.38 vs. $1.31 estimated) and revenue ($1.18 billion vs. $1.16 billion).

Its bottom line numbers also showed some significant improvement as well: $207.1 million up from $141.2 million in the same quarter a year earlier.

Surprisingly, the stock sold off on the news.

But the company recently announced a major shift in its business direction. It dropped the word “Video” from its company name to signal its expansion into the field of AI.

In reaction, the company is introducing a number of artificial intelligence (AI) features. It recently unveiled its AI-first Work Platform designed to help enhance interaction and productivity through AI tools. This includes its Zoom AI Companion 2.0, an AI assistant that can perform tasks such as summarizing conversations, identifying action items, and helping compose messages.

And the company has plans to introduce more AI-driven features, designed to target specific industries.

Leveraging AI functionality in their software could be a critical move in an age of exponentially growing digital data.

Zoom Communications (ZM)

Source: Barchart.com

While it may never see its lofty all-time highs again, Zoom could be rebuilding for a Cisco-style comeback.

And it may now be a stock worth watching…

They’ll never say it out loud, but the position of Treasury Secretary is basically your mom.

The high-profile, cabinet-level position is basically in charge of paying the bills, collecting the income and managing the finances — pretty much like your mom did way back when.

Unlike your mom, the Treasury Secretary is also in charge of overseeing national banks, printing currency (not like the Fed, but actually printing and minting bills and coins), enforcing financial laws and prosecuting financial criminals and tax evaders.

These are all important jobs. But one of the most important that your mom also doesn’t get to do is weigh in on fiscal policies. Fiscal policy refers to how the government spends its money.

As the government doesn’t actually “create” value, it doesn’t really “earn” money. So for the record, fiscal policy is how the government spends other peoples’ money.

To obtain this money, the Treasury Department levies taxes on its citizens. And what that money can’t cover, they borrow.

Since the turn of the millennium, there have been eight people from both sides of the aisle to hold the office. During that same time, the national debt has increased by 523%.

Thanks to this irresponsibility two major credit rating companies downgraded the US’ credit rating under the terms of Timothy Geithner in 2011 and Janet Yellen in 2023.

(That is terrible fiscal planning that threatens our economy overall.)

So when a new Treasury Secretary is nominated, markets generally have a say…

The New Guy on the Hill

Recently, President-Elect Trump nominated Scott Bessett to take over the job in his administration.

FILE – Investor Scott Bessent speaks on the economy in Asheville, N.C., Aug. 14, 2024.(Matt Kelley | (AP Photo/Matt Kelley, File))

The following Monday, the Dow Industrials erupted, soaring as much as 519 points on the news.

It would seem the market approved. Bessent does represent a change from the current Treasury administration.

Janet Yellen has been a lifelong academic and a career bureaucrat.

Bessent on the other hand, has a background in the market. The letters behind his Yale degree only reach to BA (but he was a member of the Wolf’s Head Society — one of Yale’s three “secret” societies — so that’s gotta count for something).

He basically made his bones in the market working for Soros Fund Management (yes, that Soros) where he was on board during the Black Wednesday crisis where his boss crushed the British Pound.

He left Soros in 2000 to start his own hedge fund which shut down in 2005. He returned to Soros where he stayed until 2015 when he went off to start another fund, the Key Square Group.

While some may wonder about his Soros-related pedigree, he is a guy with in-the-trenches experience in financial markets.

A Deeper Look

Bessent is a “macro” investor — a strategist who considers macroeconomic and geopolitical factors — which gives him a real-world perspective on what works and what doesn’t where the economy goes.

Among his stances around the incoming president, he’s promised to take action on Trump’s tax cut plans. Including “making his first-term cuts permanent, and eliminating taxes on tips, social-security benefits and overtime pay.”

He’s been a vocal critic of the US’ debt load which the bond market should find interesting. In a plan to help get the debt under control he’s promoted the ideas of reducing government spending. And freezing non-defense discretionary spending.

This will be an important focus as Congress will have to re-implement the debt ceiling it suspended in 2023.

He’s also proposed an economic policy he calls “3-3-3.” According to the Wall Street Journal:

Bessent’s “three arrows” include cutting the budget deficit to 3% of gross domestic product by 2028, spurring GDP growth of 3% through deregulation and producing an additional 3 million barrels of oil or its equivalent a day.

But most notable is his stance on Trump’s tariff policies.

Tariffs have been the most controversial aspects of Trump’s economic plan. Opponents have called it mercantilist and protectionist promising higher costs for consumers.

Bessent backs Trump’s ideas on tariffs, just not all at once. Taking a more gradual approach, “Bessent said he favors that they be “layered in” so as not to cause anything more than short-term adjustments.”

Bessent called for tariffs to resemble the Treasury Department’s sanctions program as a tool to promote U.S. interests abroad. He was open to removing tariffs from countries that undertake structural overhauls and voiced support for a fair-trade block for allies with common security interests and reciprocal approaches to tariffs.

Seeing Bessent as a backer and a balance for the incoming POTUS, the market has approved of the choice thus far.

Nevermind that so many retailers have their Christmas decorations out and for sale sometime around Halloween (or even earlier!)

Things don’t start heating up until the day after Thanksgiving.

The day that has infamously become known as “Black Friday.”

The shopping version of the day started back in the 80s. In theory it’s the day retailers went from “in the red” to profitably “in the black.” And to kick off the holiday shopping season, they offered some of the most irresistible deals ever.

Sometimes opening in the middle of the night, retailers would open their doors to “hordes” (and we do not use that word hyperbolically) of bargain hunters stampeding in to get their hands on one of the limited number of big screen TVs, or computers, or gaming consoles…

It made for some riveting images over the years…

Source: Getty Images

With the ascendency of Amazon, online shopping began to steal some of Black Friday’s thunder and Cyber Monday was born.

The span between the two days has become a critical barometer for how the larger shopping season will go. And ultimately how retailers will perform during what’s become a really critical season for profits.

This year may be even more telling.

Predictions of a Booming Season

Management consultancy Bain & Company has prepared some predictions for this year’s holiday shopping extravaganza. First the good news…

Retailers can expect another doorbuster Black Friday–to–Cyber Monday shopping period. Bain forecasts US retail sales will reach $75 billion for the first time ever, growing by about 5% year over year and outpacing our total holiday season forecast of 3%. What’s more, around 8% of Bain-defined holiday sales will come between Black Friday and Cyber Monday this year—the highest share since 2019. This underscores the enduring importance of this key shopping weekend.

Further, they anticipate that 8% of all holiday sales will be made during that weekend.

A big kickoff to the shopping season is a key signal for retailers. Over the past three years, Black Friday has ranked either first or second in terms of sales made over the period. (Over the past two years, Cyber Monday has dropped out of the top-7 sales rankings.)

A softer start to the season would not bode well for retailers and increase pressure to boost sales during the 2-3 days before Christmas — another popular shopping window.

Still the initial outlook is bright.

Something Else to Watch…

We hate to be a total Grinch during this festive season, but the actual consumer is something else we need to watch. Simply because they’re spending in record amounts, shouldn’t be interpreted as a booming consumer sector.

Financial website NerdWallet recently published its holiday spending report. Right in line with the Bain report, their feedback has been positive.

The holiday season is nearly here and with it, ample opportunity to spend big. According to a new NerdWallet analysis, Americans plan to spend about $17 billion more on gifts and about $46 billion more on flights and hotels this holiday season than they did last year.

Unfortunately, what this survey doesn’t tell us is whether shoppers plan to buy more things or just anticipate paying higher prices. Or some combination of both. Still, more money spent is generally good for the retail sector.

One thing the study does indicate is how consumers are paying for all their holiday joy.

Most shoppers plan to use credit cards again for this year’s holiday shopping: Nearly three-quarters of 2024 holiday shoppers (74%) say they’ll put at least some of their holiday gift purchases on a credit card.

More and more shoppers are relying on credit to make purchases.

And while some shoppers use their plastic to earn some type of reward, suggested by the number of shoppers who quickly pay off their balances…

Of Americans who put 2023 holiday gift purchases on a credit card, less than a third (31%) paid it off with the first statement.

…Others use them out of necessity evidenced by lingering balances:

The survey found that nearly 3 in 10 Americans who used credit cards to pay for holiday gifts last year (28%) still haven’t paid off their balances. Likewise, the same proportion (28%) of 2023 holiday travelers who put flights and hotel stays on a credit card still haven’t paid off the balances.

We’ve been writing about the struggles of the average consumer and how it’s been showing up in the retail sector. Certain retailers (Walmart, Costco…) are booming while others (Target, Kohls, and most dollar stores…) have been getting the cold shoulder from consumers.

Retailer’s earnings fate in the coming quarter will depend largely on how holiday sales go.

The economy, on the other hand, is far more dependent on the fate of the consumer…

Is he a modern-day Leonardo da Vinci?

Or just a master grifter?

Everyone has an opinion about Elon Musk.

But whether you love him or hate him, you have to admit that opportunity always seems to follow wherever he goes.

Musk has been at the helm of Tesla (NASDAQ: TSLA) for nearly 20 years. And in that time, amid unkept promises and years-late deliveries, he’s still managed to grow Tesla into the most valuable car manufacturer in the world — in most cases by a factor of 10!

And not simply because of the cars it makes. But because of the technological opportunities that the company (and Musk) creates.

Tesla makes cars. But it’s also a software company. It’s a robotics company. It’s a battery company.

And no matter how fast traditional car makers try to play catch up, they’re still a long way off from what Musk is serving up. (None have generated any significant profit from the EV segments.)

And now, his sudden “bromance” with President-elect Trump has once again put Musk and Tesla in the spotlight.

Trump has gone on record saying he’s not a fan of the Biden administration’s “EV mandate.” But, notably, his tone has softened since the “First Buddy” helped deliver a decisive electoral victory in November.

The market seems to understand this because since Musk endorsed Trump, Tesla’s share price has rallied substantially.

There looks to be a great deal of opportunity coming on the heels of this “merger.”

But there are other strategic ways to capitalize on the Trump/Musk trend besides Tesla…

Playing the Tesla Wave Strategy #1: Large Cap

While Tesla is the 800-pound gorilla of the EV manufacturing world, one US player is starting to play some serious catch-up.

Rivian Automotive (NASDAQ: RIVN) is an exclusive EV manufacturer with a market cap of just over $11 billion.

The company struggled out of the gate like any other EV company has, but today they’re making great strides in growing their business overcoming production delays and delivering vehicles on a regular schedule.

Currently they only produce two models of vehicles: the R1T and R1S.

And in doing that, they’ve actually done one strategically smart thing… They opted to specialize in producing the most popular vehicle type in the US, trucks and SUVs.

Trucks and SUVs continue to be the most popular type of vehicle in the United States. Sales of trucks and SUVs were up 17.2% in August 2023 from August 2022.

This carves out a niche for them to become top competitors to Tesla’s Cybertruck.

To make their vehicles even more attractive, they’ve made their chargers compatible with Tesla’s Superchargers giving their users more options for charging when on the road.

Additionally, they’ve partnered with Amazon to deliver 100,000 electric vans by 2030 giving them a solid demand base for the coming years.

Most recently, In November 2024, the Biden administration announced a conditional commitment for a $6.6 billion loan to Rivian Automotive to support the construction of a new electric vehicle (EV) manufacturing facility in Georgia.

The planned facility, known as Project Horizon, is expected to produce up to 400,000 vehicles annually and create approximately 7,500 jobs by 2030. Rivian intends to manufacture its more affordable R2 and R3 models at this plant, targeting a broader consumer market.

Their price action has tracked Tesla’s over the past year but has lagged since “Trump/Musk” rally. Now may be their opportunity to catch up.

Rivian v. Tesla

Source: Barchart

Playing the Tesla Wave Strategy #2: Mid Cap

While Tesla typically makes people think of car manufacturers, battery technology remains the heart and soul of the EV revolution.

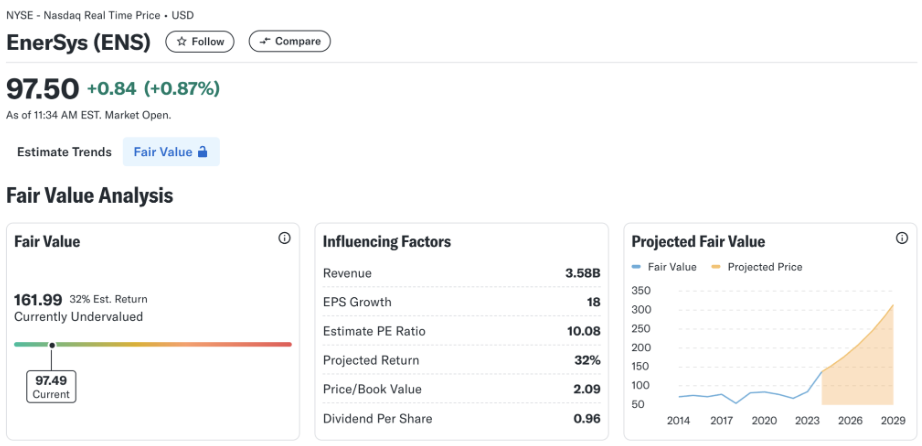

Enter EnerSys (NYSE: ENS), a mid-cap company specializing in energy storage solutions. Known for its innovative battery systems, it’s a critical supplier for both the EV and renewable energy sectors.

As of December 2024, EnerSys boasts a market capitalization of $3.83 billion, with its stock trading at $96.66 per share. Its steady growth and diverse product portfolio make it an ideal choice for investors seeking stability with upside potential in the rapidly expanding EV battery market.

What’s more, according to a Yahoo Finance Fair Value analysis, the company is currently significantly undervalued, with a potential 32% upside according to the web site’s analysts.

Source: Yahoo

Playing the Tesla Wave Strategy #3: Small Cap

Rivian and EnerSys are both solid, well-capitalized players in the traditional EV world.

But for investors with a bit more risk appetite, you’ll want to look at smaller-cap companies looking to add a disruptive aspect to the rapidly growing sector — a company looking to bring something entirely “new” to the game.

These are the companies that offer the potentially biggest bang for your investment buck.

And if that’s what you’re looking for, Nuvve Holding Corp. (NASDAQ: NVVE) is well worth considering.

Nuvve’s breakthrough technology is called Vehicle-to-Grid (V2G) technology.

V2G is a smart charging technology that effectively allows EV batteries to resell stored unused power back to the grid — effectively making any EV owner a power provider. This innovative “personal grid” technology could well revolutionize how power is managed and monetized.

And this kind of forward thinking couldn’t come at a better time. Given the exponential demands for electricity that the AI megatrend is placing on grid and grid infrastructure, this kind of technology could be rapidly viewed as a major solution to the problem, and one that could be implemented right now without significantly overhauling the existing grid infrastructure.

Currently, Nuvve has a market capitalization of just $3.19 million. But despite its small size, the company has been making strategic moves to position itself as a major player in the nascent but rapifly growing V2G market.

While small-cap stocks carry inherent risks, Nuvve’s potential to tap into the multibillion-dollar V2G market gives it a growth trajectory that few other companies can match.

The Trump/Musk relationship has made a huge splash in the business and political industries …

… But it’s these three companies that could well be riding the wave higher.

Let’s cut to the chase…

This week on Investment Journal we’ve been contemplating the questionable state of the US consumer. And if their state really is questionable, that calls into question the future state of retail players throughout the economy.

It’s no secret to anyone paying attention that retailers have been facing their share of struggles since the pandemic.

Over the course of 2024, and with the S&P 500 up just over 25% year-to-date, some have worked their way higher. For instance…

Home Depot is up nearly 21% while Kroeger is up 28%. The Gap, who struggled through some volatility, is up 16%. And Best Buy is up just over 15%.

Others, however, have struggled…

CVS and Walgreens are off 28% and a disappointing 67% respectively. Macy’s is down 17% and Kohls is off 39%. Target recently took it on the chin giving up all its annual gains, now trading some 13% lower.

But then there are those who have outperformed like BJs Wholesale Club up 44% and Costco up a very solid 48%.

But none of these can touch Walmart — up a stellar 70% on the year.

Walmart vs. S&P 500 (YTD)

Source: Barchart

So is WMT the NVDA of retail?

To Dominate in Retail…

Walmart’s surge comes on the heels of a series of positive earnings reports. Most notably was last week’s earnings:

• Earnings per share: 58 cents adjusted vs. 53 cents expected

• Revenue: $169.59 billion vs. $167.72 billion expected

But not only that, they upped their guidance for the year looking for sales to grow between 4.8% and 5.1% versus their previous forecast of between 3.75% and 4.75%.

We noted this week that a sizable portion of that growth (75% of the gain) was from households earning over $100K per year. Not what you’d consider to be a typical Walmart shopper.

Clearly Walmart has been a force in the discount retail sector for years. But why have they been so dominant, attracting a higher income cohort while others (like Target) can’t keep up?

We think it’s because they’re a superior company. And here’s what we mean…

Like most of the competition, early on in 2022 WMT was struggling to rebound from the disaster that was the pandemic shutdowns. Their stock dropped nearly 25%. But by the end of the year they started to rebound while the competition lagged.

One of the main reasons?

Management!

They were better able to manage inventory issues that had arisen out of the pandemic. They were able to cut their Inventory overhang by more than $500 million in just one quarter by strategically discounting prices.

This faster path back to normal was in large part thanks to better management.

And that same savvy management has them over performing this year.

The Nvidia of retail?

We’ll see…

The US consumer is the bedrock of our economy.

If that’s truly the case — (and it is) — then signals are flashing everywhere that the economy is headed for trouble.

Case in point…

Source: ZeroHedge

The Tylers over at ZeroHedge reported:

Bloomberg Intelligence’s Joel Levington published a new report Monday, citing new data from CarEdge that showed a staggering 39% of vehicles financed since 2022 carry negative equity, including 46% of EVs…

What this basically means is that balances on people’s auto loans are more than the value of the vehicle they’re paying on.

Now falling car values shouldn’t come as a surprise to anyone.

A car is not an asset in any “investment” sense of the word. It’s a means of transportation.

In the world of business, vehicles are recognized as “depreciating assets” (over the “useful life” of the vehicle) on a business’ taxes. They have a tax-reducing effect on their bottom line.

Depreciation refers to the decrease in value of long-term assets over time. Depreciation is spread over the useful life of the asset and is intended to realistically reflect the actual value of the asset and the profit. Furthermore, it is designed to have a tax-reducing effect. Depreciation of vehicles is done on a linear basis, meaning the vehicle’s value is evenly spread over its useful life. The vehicle’s useful life plays a crucial role in this process. The amount of depreciation depends on the purchase price and the vehicle’s useful life.

There’s a maxim that says cars depreciate by over 10% the minute you drive it off the dealer’s lot. So you’re pretty much starting in the hole.

So, again, the fact that the value of American’s cars are falling shouldn’t be any surprise. What is troubling is the fact that consumers still owe so much on their vehicles.

Consumers Are Sinking Fast

The Federal Reserve just reported that the average finance charge for a new car in Q3 2024 was 8.76%! But that’s not the really shocking part. What really catches your attention is that’s the rate being charged for a 72 month loan!

Six years to pay off a car? Not long ago four years was pretty much the financing limit.

The problem stems from a combination of factors.

Back during the pandemic stimulus spree, the extra free money (not to mention the near zero financing cost) at the time made trading in the old car seem like a good idea.

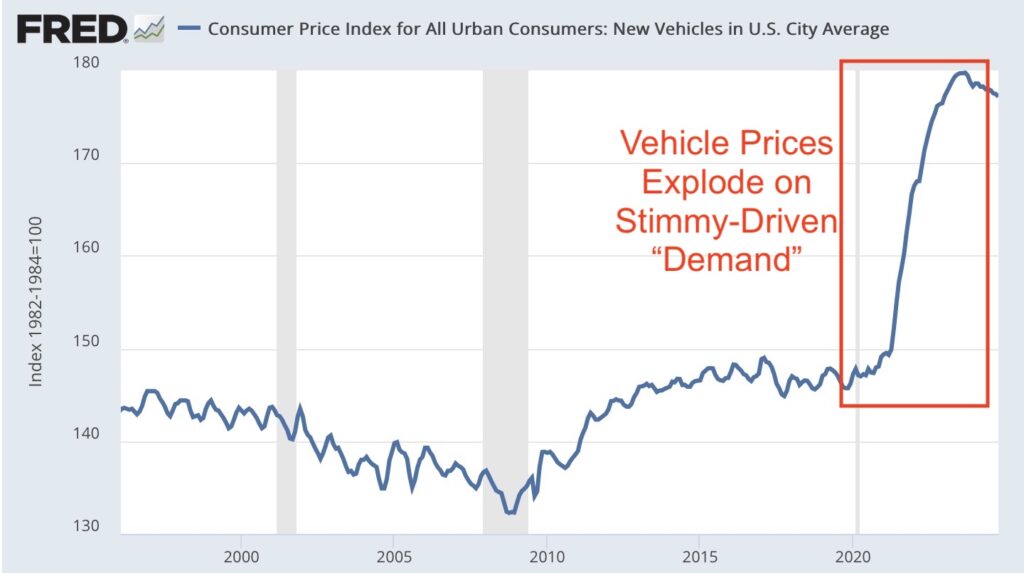

The stampede to the local car dealer (along with the supply fiasco) drove new car prices through the roof.

Source: Federal Reserve Bank of St. Louis

After some 20-plus years of relative price stability in the new car market, prices exploded by over 20% in a span of three years thanks to all the “free” money.

Today, thanks to the sharply higher prices, auto loan balances rose by $18 billion in the last quarter alone, and now stand at $1.64 trillion — the highest category of non-housing debt.

These unaffordable prices are what’s behind the longer and longer financing terms.

Further according to Experian 33% of monthly car payments stand between $500-$700 per month. And, hold on to your hats, over 16% are over $1,000.

This would be fine if everyone could afford it. But 90-plus day delinquency rates on auto loans just upticked again to 4.6%. (Which might not seem bad compared to credit card delinquencies which have reached 11.1%!)

There’s an idea floating around that the economy is doing just fine.

But when you look past the headlines (and you don’t have to look far) you can see the strains building.